2025-01-12

consider a trader who is backtesting a series of alphas that target the 30 DTE contracts on the S&P 500 Index options chain. to increase sample size, the trader uses a window of +/- one day from the target.

the trader considers the following:

in order to avoid adding complexity where unncessary, the trader starts question the premise:

through the selectively biased lens of my day-to-day experiences, it seems increasingly more common to default to thinking instead of thinking. stated another way, there seems to be an upward trend of .

for clarity, thinking is not the same as thinking. in my mental model, thinking is a subset of thinking:

of course, thinking is represented in a reductive manner above; to capture the notion that a human supervises the , let us expand the notation a bit:

the expression of simply captures:

for example, one might say that someone who blindly accepts machine reasoning has :

furthermore, by definition, thinking blindly rejects machine reasoning i.e. :

while i am admittedly a staunch contrarian when it comes to the topic of LLMs, i do concede they have realized utility in some applications. my intention is not to debate the utility curve of LLMs; rather, i aim to invite deeper thinking about effects of human-LLM interactions.

may be perfectly valid in some contexts, but not all contexts. what i worry about most is that continuous exposure to in valid contexts erodes the human detection mechanism responsible for drawing that line in the first place.

as of writing, machines cannot reason from first-principles; therefore, humans must become more resilient in explicitly protecting the spaces in which may lead to less than ideal outcomes. a serendipitous, cherry-picked personal example follows for those interested in virtually useless proofs.

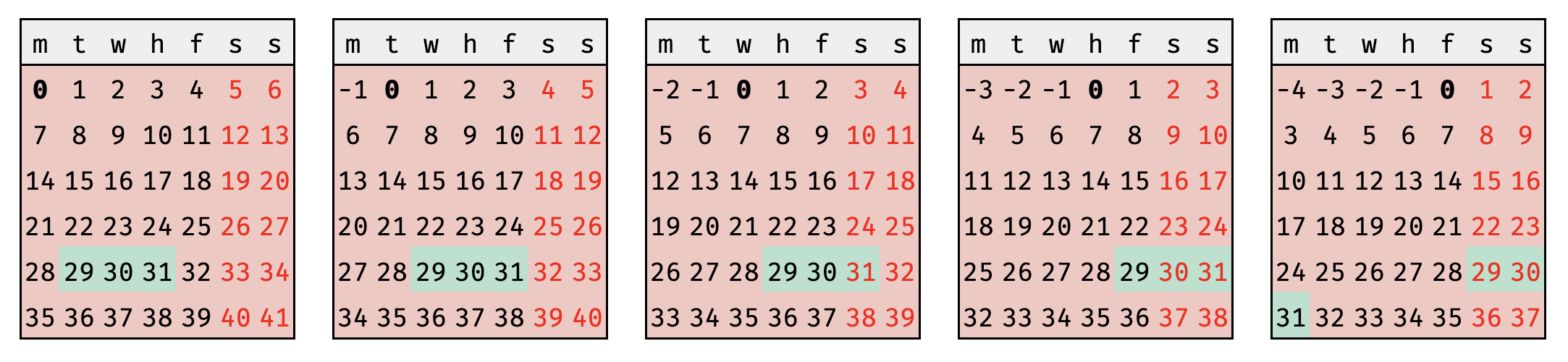

if one were to take trading days and weekends as such:

if today and target DTE , one might observe that deriving day of the week for is simply:

for 30 DTE strategies, one is never presented two equivalent choices for days-to-expiry in non-holiday conditions.

using the above, one observes when the possibility of a choice may arise:

that is to say, a choice may only happen on Thursday or Friday. given, two choices: and representing 29 DTE and 31 DTE, respectively:

thus, is always presented while is always presented .

using to indicate the current trading day, there exists a nice visual proof; make note of when (thursday) is the current day and (friday) is the current day .

questioning assumptions and re-stating base truths often can combat misguided efforts, such as adding complexity where none is required. this is the essense of thinking that must continue to be protected in the age of .

as always, it is helpful to take a step back every now and then and ask,

note: in no way are the results below meant to be cherrypicked, i do not pay for any LLM services. as such, the results below are derived using the "smartest" free model i could select.

additionally, there's usually more than one way to do the same thing; i am sure there exists a " power user" who could likely construct the proof above (or some similarly acceptable proxy of the proof) in a similar amount of time that i spent constructing it ... perhaps even shorter?

Prompt

SPXW options have 5 daily expirations (Monday-Friday) I want to trade an options strategy that buys 30 DTE contracts, but I want to include +/-1 day in my range (29-31 DTE) to ensure I get enough samples when 30 DTE isn't available.

Give me a list by weekday (Monday-Friday) of which expiries (29, 30, 31 DTE) are available.

ChatGPT Response

Monday

Tuesday

Wednesday

Thursday

Friday

Notes:

Gemini Response (2.0 Flash)

Here's a breakdown of the available SPXW expirations (29, 30, and 31 days to expiry) by weekday: